Category: Market

2025-2027 Canadian Housing Market Outlook

Canada’s housing market is at a crossroads. The CMHC’s latest 2025 report reveals a mix of challenges and opportunities for real estate investors, particularly those eyeing rental properties. Let’s cut through the noise and break down what this means for your portfolio.

What Investors Need to Know

1. Mortgage Rates Are Dropping—But Not for Everyone

The Bank of Canada is expected to trim interest rates in 2025, making variable-rate mortgages more appealing. However, fixed-rate loans won’t see dramatic dips, so investors should weigh short-term savings against long-term stability.

2. Condos Are Cooling, Rentals Are Heating Up

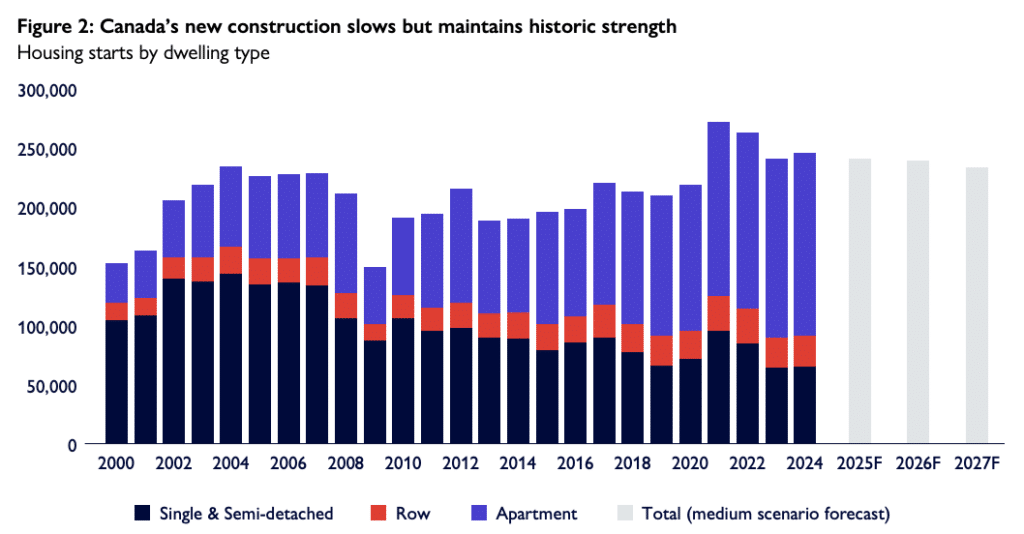

Condo construction is slowing nationwide (thanks to weak presale demand), but purpose-built rental apartments are booming. Governments are throwing cash at rental projects—think tax breaks and faster permits—making this segment a safer bet.

3. Vacancies Are Rising, But Don’t Panic

More supply means vacancy rates will creep up, especially in cities like Toronto and Vancouver. Still, rents aren’t crashing. Why? Inflation and demand for modern units keep upward pressure on prices.

Where to Invest: Top Markets to Watch

1. Toronto’s Suburbs: The 905 Is King

The Opportunity:

Condo projects in downtown Toronto are struggling, but suburbs like Mississauga and Brampton are goldmines for rental apartments. Developers here get more bang for their buck, and tenants flock to family-friendly neighborhoods.

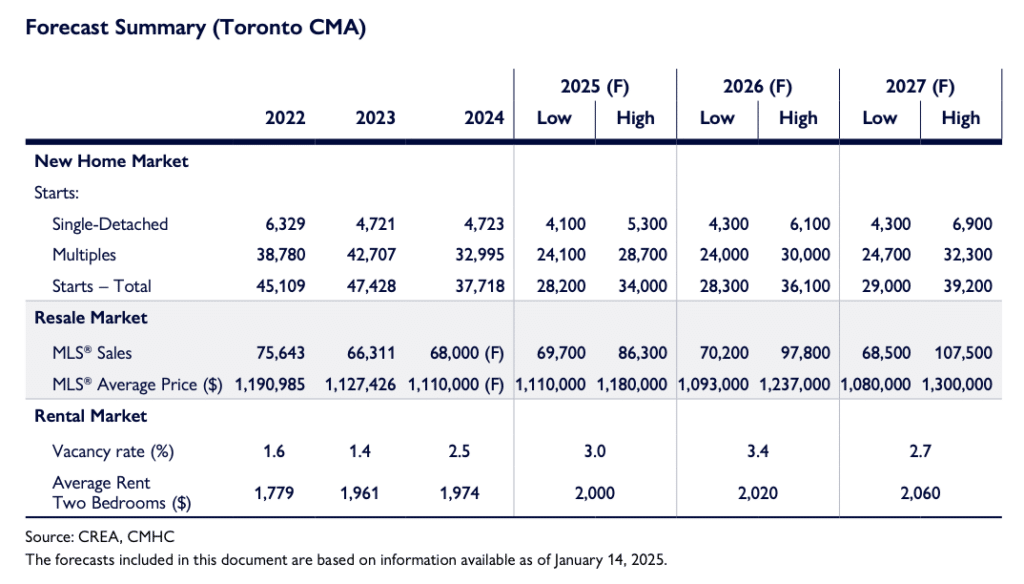

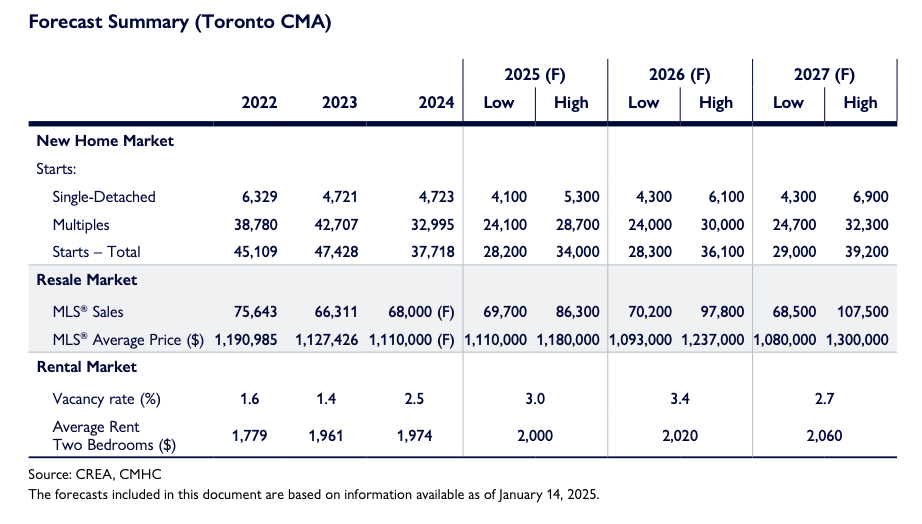

Average rents for 2-bedrooms will hit $2,060/month by 2027—up 4% annually.

The Catch: Land costs are rising in the 905, so act fast. Look for properties near transit hubs or upcoming infrastructure (e.g., the Ontario Line extensions).

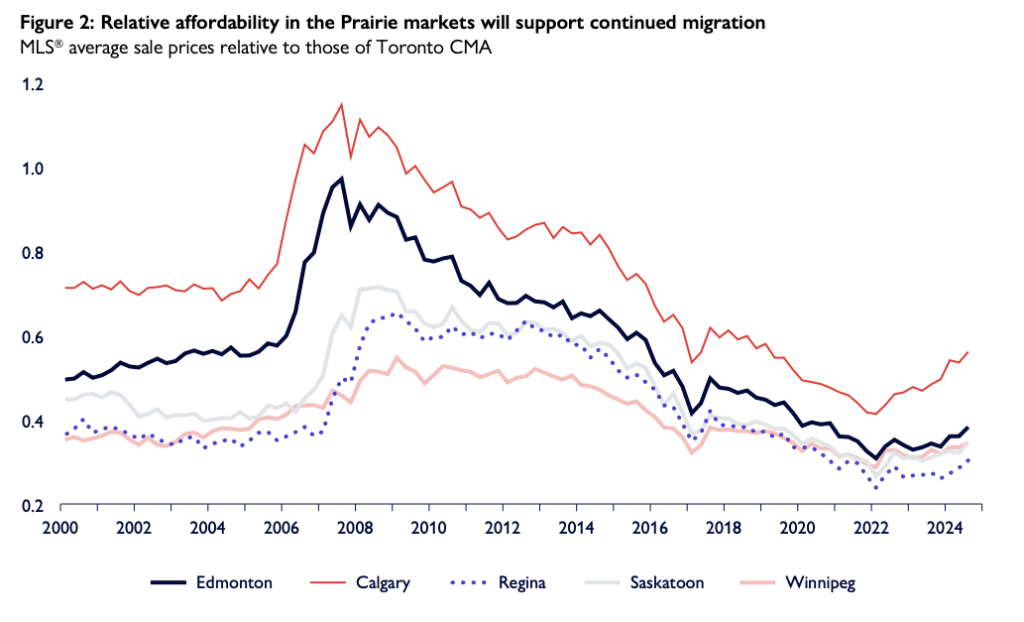

2. Alberta’s Hidden Gems: Calgary and Edmonton

Why It Works:

- Calgary’s population is exploding (thanks to relocations from pricier cities), yet prices here are still 40% lower than Toronto’s. Single-family homes and duplexes are in high demand.

- Edmonton’s rental market is loosening, but investors can still score 5-6% annual returns on well-located units.

Pro Tip: Alberta’s lack of rent controls means you can adjust rates freely—a perk if you’re renovating units to attract higher-paying tenants.

3. Quebec and Atlantic Canada: Steady Wins the Race

- Montréal: Vacancy rates hover near 2%, and rents are climbing steadily. Focus on neighborhoods like Griffintown or Verdun, where young professionals dominate.

- Halifax: Limited supply and a growing tech scene make this a sleeper hit. Just brace for slower construction timelines—local labor shortages are real.

Red Flags: Risks to Keep on Your Radar

Immigration Cuts: Fewer international students = emptier units near colleges. Avoid investing in “student ghettos” like parts of Brampton or Scarborough.

Trade Wars: If U.S. tariffs hit Canadian exports, manufacturing-heavy regions (e.g., Windsor, Hamilton) could see job losses—and softer housing demand.

Condo Glut: Toronto’s downtown core has a 12-month oversupply of unsold condo units. Steer clear of pre-construction here unless it’s a fire-sale price.

3 Actionable Strategies for 2025

- Swap Condos for Rentals: Use government incentives (like GST rebates) to build or buy purpose-built apartments. Bonus: Tenants stay longer in these units.

- Go Small in Secondary Cities: London, ON, or Winnipeg offer cap rates over 6%—way higher than Toronto’s 3-4%.

- Lock In Rates Now: Refinance variable loans to fixed rates while lenders are still offering sub-5% deals.

Conclusion

The next three years will reward investors who adapt. In Toronto, that means ditching condos for suburban rentals. Out West, Alberta’s affordability is a magnet for cash flow. And if you’re risk-averse? Québec and the Maritimes offer slow-but-steady gains.

How does the Federal 2024 Budget impact investors?

The 2024 Federal Budget proposes a number of changes that have caused an uproar among voters and the LinkedIn community. We decided to discuss the changes and how they impact Real Estate Investors and Developers.

At a macro level, real estate is built and funded based on free-flowing capital. Our clients seek opportunities to place their capital and realize returns on it before moving on to the next opportunity. The returns generated are then used to invest in the economy by building businesses, innovation, and creating high-paying jobs for a productive workforce.

Canada has to compete at the global level for capital, and like anyone running a business, we need to be easy to do business with. The stance taken by the Trudeau government in this budget is the opposite of pro-investment in an era of anemic economic growth and next to zero job creation by a private sector grappling with high interest rates and tightened consumer spending.

The list below does not include every single change in the budget but rather the highlights proposed and their general implications for our clients. If you’d like to explore how these tax changes impact your portfolio or your real estate firm, feel free to reach out for a complimentary consultation at info@westcliffam.com or www.westcliffam.com. We are here to help you every step of the way in this challenging environment. Our team of talented real estate tax accountants can help you navigate through these changes.

Let’s dive right into our top 5 budget changes with their impact on Real Estate Investors and Developers:

- Increase in Capital Gains Inclusion Rate

I am sure you have seen a ton of articles on this, but at a high level, this change of the inclusion rate from 1/2 to 2/3 will likely increase property sales and investment disposition activity by June 24, 2024. For my realtor and investment advisor friends out there, buckle your seatbelts!

From a longer-term perspective, this is a terrible change for anyone making investments, building a business, or planning their retirement. In short, in most cases, you will have lost an extra 17% of your after-tax cash available to either make your next investment or retire.

This change does the opposite of incentivizing more investment and productivity, making tax compliance much more complicated!

2. Lifetime Capital Gains Exemption (LCGE) and Canadian Entrepreneur Incentive

Generally, this change provides additional opportunities to shelter more of the capital gains on the disposal of qualifying small business shares under certain conditions. Unfortunately, the incremental change doesn’t necessarily offset the negative impact of the increased inclusion rate in capital gains.

3. Home Buyers Plan Withdrawal Increase

Do first-time home buyers have extra cash in their RRSP to buy a property? Well, if you are one of the rare bunch who do, you can take out $60K per person instead of the $35K you can today with a 3-year deferral on repayment.

Similar to other incentives for home buyers, the main challenge is that we need more homes for them to purchase and more higher-paying jobs to give them the cash flow to qualify for these purchases.

4. Higher CCA on Purpose Built Rentals

Typically, buildings have a 4% tax depreciation and a half-year rule for the first year of putting them into use. You will now be able to write off 10% tax depreciation (CCA) for buildings constructed starting April 16, 2024, with move-ins by January 1, 2036. An additional incentive here is that there is no half-year rule if you put the building in use before 2028.

Unfortunately, these benefits aren’t realized until after you have built the building and are in the leasing up stage, which usually has lower income in the first year. The real challenge developers are having is to get a handle on the full costs of buildings, making a market profit, and ensuring the capital stack is viable. In most cases, this is a down-the-road benefit and doesn’t help us get more buildings built.

5. Higher CCA on Patents and Technology

In an effort to incentivize businesses to invest in patents and technology, the Feds have increased tax depreciation rates from 25%/30%/55% to 100% if purchased on April 16, 2024, and put in use by January 1, 2027.

This may help industries that spend a lot on technology and patents, so I will leave it to experts in those fields to give their opinions. From a real estate perspective, most of the software has moved to SAAS, and so the software is being paid for and written off as an expense during the contract, resulting in little to no impact. For those in the prop-tech space, this could be a great benefit!

You can find more information on the 2024 Canadian Federal Budget here.

Our team would be pleased to discuss how these changes impact your portfolio and real estate investment strategy. Feel free to reach out at info@westcliffam.com or www.westcliffam.com.